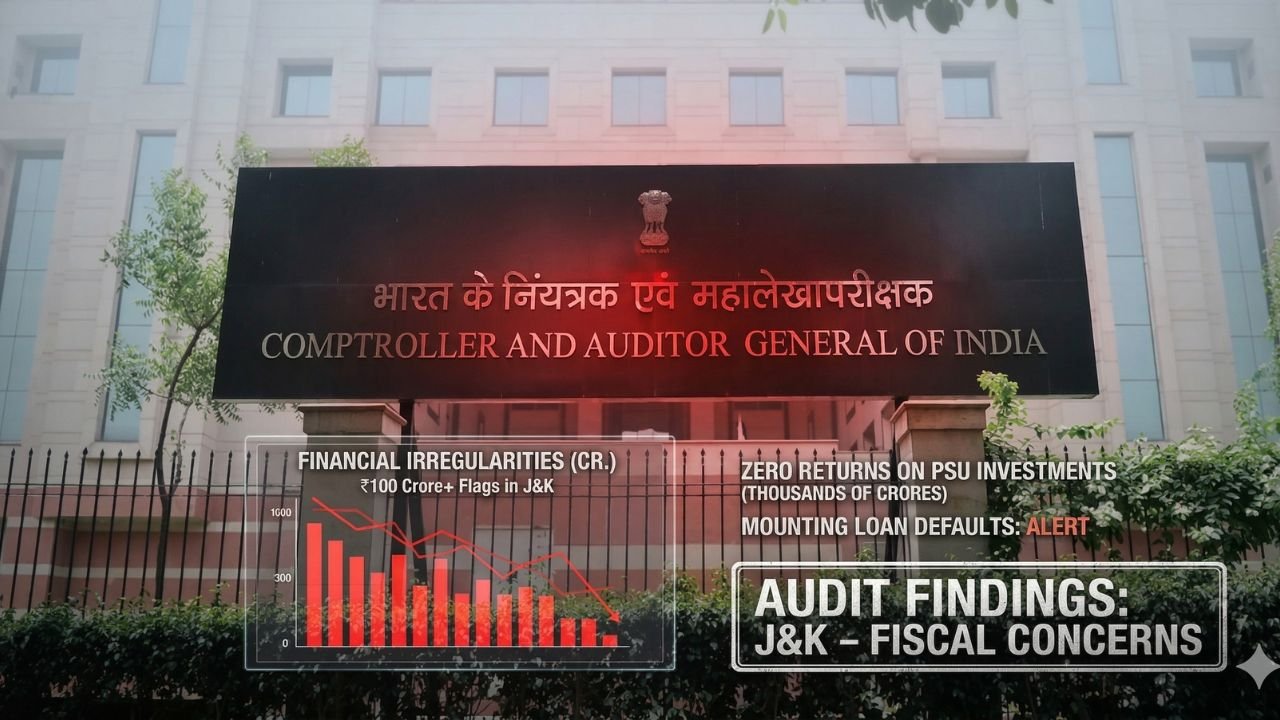

The Comptroller and Auditor General of India — the country’s highest constitutional audit authority — has placed Jammu and Kashmir’s Government financial management under an uncomfortable spotlight. In audit reports recently tabled by Chief Minister Omar Abdullah on the floor of the J&K Legislative Assembly, the CAG has documented a pattern of financial irregularities, poor investment returns, slow loan recoveries, and growing fiscal inefficiency that spans multiple years and departments.

The findings go beyond routine audit observations. They paint a detailed picture of how public money has been deployed, what it has returned, and where the gaps between intent and outcome have widened — often at significant cost to the taxpayer.

₹104 Crore Flagged: The Core Financial Irregularities

The headline finding of the CAG report is the identification of financial irregularities exceeding ₹100 crore across Jammu and Kashmir’s Government. The audit has broken this down into three specific categories:

Doubtful Recovery — ₹104.51 Crore: This is the largest and most significant figure. Money classified as “doubtful recovery” refers to funds disbursed by the government that are now considered unlikely to be returned in full — either because the recipient organisations are financially unviable or because follow-up mechanisms have been inadequate.

Avoidable Interest — ₹6.88 Crore: This amount represents interest that the government paid unnecessarily — a direct consequence of delays in financial processing and mismanagement of fund flows. In accounting terms, this is money spent not on development but on administrative inefficiency.

Idle and Unutilized Funds — ₹2.65 Crore: Funds that were allocated but never deployed for their intended purpose. The CAG notes that money was “parked without timely utilization,” meaning development work was deferred while the funds sat unused in accounts.

As the audit observed: “Avoidable financial burden and unutilized funds reflect deficiencies in planning and monitoring.”

Experts in public finance note that while individual figures may appear modest relative to the overall budget, the patterns they reveal — poor planning, delayed execution, and weak monitoring — have a compounding effect on overall development outcomes.

52 PSUs, ₹4,031 Crore Invested — Only One Pays a Dividend

Perhaps the most striking finding in the CAG report concerns Jammu and Kashmir’s investment in its Public Sector Undertakings (PSUs). The government currently holds stakes in 52 government-owned corporations, ranging across sectors including infrastructure, transport, finance, and agriculture. The return on this vast portfolio of public investment has been, by any measure, deeply underwhelming.

Between 2020 and 2025, only one out of 52 PSUs — Jammu and Kashmir Bank — paid any dividend to the government. Every other corporation in the portfolio generated zero return on the public capital invested in it.

For the financial year 2024–25, the government’s total investment in PSUs stood at ₹4,031.25 crore. Against this, J&K Bank returned a profit of ₹130.78 crore — representing a return of just 3.24 percent on total invested capital.

To put this in context: the government is simultaneously borrowing money at an average interest rate of 8.82 percent. It is paying more than eight rupees in interest for every hundred rupees it borrows, while earning barely three rupees in return from the companies it has invested in. The CAG has described this gap as a significant and sustained inefficiency in the deployment of public capital.

Five Years of Investment in PSUs of J&K Govt, Five Years of Near-Zero Returns

The CAG report provides a year-by-year breakdown of PSU investment and returns that makes for sobering reading:

| Financial Year | Total Investment (₹ Crore) | Return Received (₹ Crore) | Return % |

|---|---|---|---|

| 2021–22 | 5,499 | 0 | 0% |

| 2022–23 | 5,932 | 0 | 0% |

| 2023–24 | 6,394 | 30 (J&K Bank) | 0.47% |

| 2024–25 | 4,031.25 | 130.78 (J&K Bank) | 3.24% |

In three of the four years examined, the return on thousands of crores of public investment was either zero or negligible. The financial year 2023–24 recorded the highest-ever PSU investment at ₹6,394 crore — and yet returned only ₹30 crore, entirely from J&K Bank.

The CAG has specifically pointed to the absence of a well-defined dividend policy as a structural cause of these poor returns. Without a clear policy framework requiring PSUs to declare dividends or meet performance benchmarks, corporations have had little institutional pressure to generate returns for their primary investor — the government of Jammu and Kashmir, and by extension, its citizens.

The Borrowing-Investment Gap: ₹1,883 Crore Lost Over Five Years

The financial implication of this disconnect between borrowing costs and investment returns is substantial. The CAG has calculated that over the past five years, the gap between returns earned on PSU investments and the cost of government borrowings amounts to ₹1,883.60 crore.

In simpler terms: the government borrowed money at roughly 8.82 percent interest and invested it in PSUs that collectively returned far less — or nothing. The difference between what it paid to borrow and what it earned from investing is nearly ₹1,900 crore over five years.

This is not a theoretical accounting loss. It represents real fiscal pressure on the government’s budget — money that could have funded schools, hospitals, roads, or welfare schemes but instead covered the cost of unproductive investment.

The CAG’s interest burden data shows a steady escalation over the review period, with borrowing costs rising from 6.65 percent in 2020–21 to 8.82 percent in 2024–25 — even as PSU returns remained largely stagnant.

Loan Recovery Crisis: ₹246 Crore Outstanding, Recovery Nearly Nil

A separate but connected concern flagged by the CAG involves the government’s loans and advances to various institutions and organisations. Here too, the trend is troubling.

The outstanding loan balance, which stood at ₹35.80 crore in 2020–21, has grown steadily to ₹246.56 crore by the end of 2024–25 — an increase of nearly seven times in five years. This growth has occurred despite loans being disbursed every year, because recoveries have been minimal and declining.

The data for recent years is particularly stark:

- 2023–24: ₹11.49 crore disbursed — ₹6.04 crore recovered

- 2024–25: ₹15.09 crore disbursed — only ₹0.44 crore recovered

In the most recent financial year, the government recovered less than three percent of what it disbursed in new loans. The CAG attributes this poor recovery directly to the financial condition of the borrowing entities — primarily loss-making PSUs that are unable to repay their dues, causing government funds to become locked in what are effectively non-performing assets.

Interest income from these loans has followed a similarly discouraging trajectory. The government earned no interest income at all in 2020–21, and while figures improved slightly in subsequent years, the highest recorded was just ₹2.21 crore in 2023–24 — falling again to ₹0.70 crore in 2024–25.

The Unresolved Apportionment Problem

An additional layer of complexity flagged by the CAG concerns investments made by the erstwhile state of Jammu and Kashmir before it was bifurcated into two Union Territories in October 2019. As of March 31, 2025, an investment of ₹3,426.75 crore made by the pre-bifurcation state government remains unallocated between the UT of Jammu and Kashmir and the UT of Ladakh.

This pending apportionment means that a significant portion of the total investment portfolio — and its associated liabilities and returns — remains in a state of administrative limbo more than five years after reorganisation. The CAG has highlighted this as a matter requiring resolution to enable accurate financial reporting and accountability for both UTs.

What These Findings Mean for J&K’s Financial Future

Taken together, the CAG’s audit findings point to a set of interconnected structural issues in Jammu and Kashmir’s financial governance:

Weak PSU accountability: With no dividend policy and 51 of 52 PSUs generating zero returns over five years, the government’s role as an investor in public enterprises needs a fundamental review.

Rising borrowing costs meeting falling returns: Borrowing at 8.82 percent to invest in entities returning near zero is arithmetically unsustainable over the long term.

Loan recovery mechanisms are failing: Outstanding loans have grown sevenfold in five years, with recovery rates collapsing to near zero in 2024–25.

Planning and monitoring gaps: Idle funds, avoidable interest, and doubtful recoveries all point to weaknesses not just in execution but in the upstream processes of planning, monitoring, and follow-up.

Legacy bifurcation issues unresolved: The unallocated ₹3,426 crore investment is a governance gap that has persisted for over five years without resolution.

The report is now before the J&K Legislative Assembly, and its findings are expected to prompt detailed scrutiny of departmental financial practices, PSU governance frameworks, and the mechanisms through which the government monitors the use and return of public funds.

CAG reports are constitutional instruments of accountability — they do not prescribe solutions but they establish a factual record that lawmakers, administrators, and citizens can act upon. The tabling of this report by Chief Minister Omar Abdullah in the Legislative Assembly marks the beginning of a process that should ideally lead to specific corrective measures: a dividend policy for PSUs, stricter loan recovery protocols, faster utilization of allocated funds, and resolution of the bifurcation-era apportionment backlog.

Whether those measures materialise — and how quickly — will determine whether the next CAG audit of Jammu and Kashmir tells a different story.

Note: The CAG report on Jammu and Kashmir’s finances for 2024–25 was tabled in the J&K Legislative Assembly by Chief Minister Omar Abdullah. All figures cited in this article are sourced directly from the audit report.